From Co-ops to Crypto: Why 50 Years of Alternative Exchange Systems Keep Failing (And How AI Might Change That)

A Veteran's Journey Through the Mutual Credit Wilderness - And a New Hope for Breaking the Cycle

I've been chasing the holy grail of alternative exchange systems for over five decades. From watching people manage double-entry ledgers in 1970s cooperatives to working with Joe Lubin on blockchain solutions, I've seen brilliant minds and millions of dollars crash against the same behavioral barriers. Now, with AI and new distributed technologies emerging, we might finally have the tools to crack this ancient puzzle.

The £5 Billion Question That Started It All

Back in the 1970s, I cut my teeth working for one of 7,000 cooperatives operating under the Co-operative Union. We had 10-12 million active members turning over £5 billion annually - a massive economic force built on mutual aid and shared ownership. My first job involved having to understand how double-entry ledgers enabled member driven credit systems, watching how communities could create value (by aggregating their purchasing power) to enable a person to pay off the debt .

It should have worked perfectly. We had scale, trust, shared values, and sophisticated accounting systems. Yet even within this idealistic framework, the same problems kept emerging: free riders, liquidity imbalances, administrative burdens, and the constant tension between individual benefit and collective good.

That experience planted a question that has driven my quest ever since: Why do alternative exchange systems consistently fail to deliver on their promise, even when they should theoretically work?

Fifty Years of Beautiful Failures

Since those early cooperative days, I've been involved in "many initiatives at both community and large-scale levels" - each time hoping we'd finally cracked the code. The pattern is always eerily similar:

Phase 1: Brilliant people identify the problems with existing systems

Phase 2: Revolutionary solution is designed with elegant theory

Phase 3: Small-scale pilots work beautifully

Phase 4: Scaling attempts reveal the same behavioral issues

Phase 5: System stagnates or collapses, blamed on external factors

I've watched this cycle repeat across decades and technologies. When Holochain launched with its promise to switch from the blockchain-based HOT coin to HoloFuel (a mutual credit system), I was immediately attracted. Here was Arthur Brock, a systems thinking pioneer, tackling the fundamental architecture problems.

During system-wide architecture training sessions with Arthur, we discussed how these persistent problems might finally be remedied. The conceptual thinking was brilliant, but scaling beyond closed small communities remained unsolved. The old English saying applies: "The proof is in the pudding."

The Joe Lubin Reality Check

My year working with Joe Lubin at ConsenSys provided a sobering perspective on just how intractable these problems are. Here was someone willing to invest over US$10 per month in young people's attempts to solve the well-understood problems including those that have inhibited mutual credit systems from replacing fiat currencies at any meaningful scale.

The recent launch of Blockchain Linea has solved the affordable scalability aspect - we can now seamlessly process transactions cheaply at massive global scale. But the vexing root cause human behavioral issues remain as stubborn as ever. All the technical elegance in the world can't overcome the fundamental tension between individual incentives and collective benefit.

The Holochain Promise (And Reality)

Recent announcements from the Holo team (unyt) suggest some progress, and I'm genuinely excited to read any papers that identify how they've addressed the core problems. The closest I've seen to a viable approach is Adam Thompson's HoloDex model, where he uses his own currency as a unit of account to enable seamless exchange of non-related items via an order book.

This required Holochain to reach the point of high-scale, low-cost transactions - something Adam has now built a platform to deliver, and the Holo team appears to have achieved similarly. But technical capability is just the foundation. The behavioral challenges remain.

The AI Wild Card

Today, I'm "playing around with and watching what a decentralised AI Bot with bags of intelligence built in." that could deliver to enable groups of people who share a common interest to address the problems and cascading pain that impact them, This isn't just technological curiosity - AI represents the first fundamentally new tool we've had for addressing the human behavioural aspects of mutual credit systems. This newfound ability to agitate a groups economic, social and even political power to match the power of supply without the need for large capital input or permission when fused together with the saleable technology and new digital laws enabling ownership of the value based assets created can now occour.

Consider what AI could bring to the table:

Intelligent matching between supply and demand across vast networks

Reputation systems that can track and predict behavior patterns

Automated governance that responds to emerging problems in real-time

Personalized incentives that align individual and collective interests

Fraud detection and prevention at scale

For the first time, we might have technology sophisticated enough to handle the complexity of human behavior in large-scale cooperative systems to address the systemic problems that our young have to address caused by the very institutions who should be protecting us and the large utility systems that should be serving our needs and not exploiting us like health, energy, communications, banking and farming.

The Stakes Have Never Been Higher

When you examine the need and likely demand for systems that give agency to individuals and crowds, it becomes apparent that the first mutual credit system to demonstrate these problems have been solved will open the door to aggregating the economic, social, and political power of crowds that share common interests and trust each other enough to give it a go.

We're not just talking about better payment systems. We're talking about enabling new forms of economic organization that could challenge existing power structures and create new types of currencies, assets and capital using circular economics to drive and fund change.

Learning from the Pioneers

Recently, I had the privilege of facilitating a think-tank session for Sabine Wienand, who leads the cooperative at Crystal Waters Permaculture Village. Working alongside her exceptional team—people who have truly walked the talk in building successful collaborative communities—Sabine has accumulated invaluable insights for anyone venturing into this space.

What struck me most about Sabine is her remarkable ability to navigate the complex challenges that often derail alternative systems. With years of hands-on experience, she's developed an almost intuitive sense for identifying problems early and crafting practical solutions or clever workarounds.

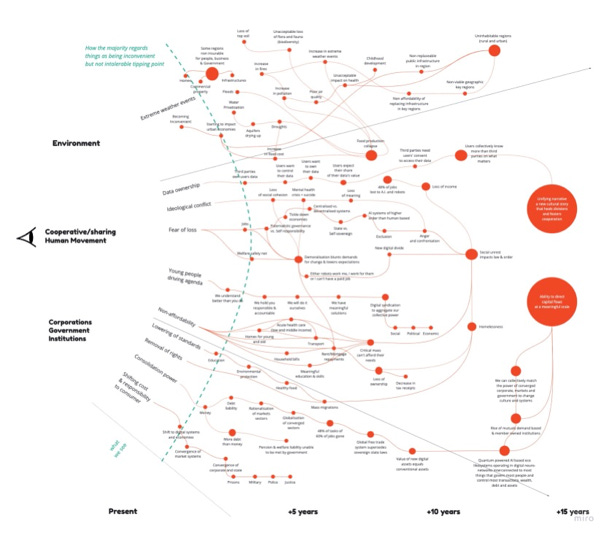

The session brought together diverse expertise, including Manu, a true innovator in decentralized technology. Together, we developed what we called a "tipping map"—a visual framework that identified the key disruptions facing traditional cooperative structures and mapped the emerging sharing economy forces reshaping their landscape.

Sabine's central question was compelling: How can those with decades of hard-won cooperative experience effectively mentor and support young people who are exploring entirely new collaborative models?

What emerged from our mapping exercise was profound: we're standing at a historic inflection point where traditional cooperative wisdom—tested through decades of real-world application—could finally merge with today's technological capabilities to create something genuinely transformative.

This convergence feels both inevitable and urgent. The timing couldn't be more critical.

Map by kind permission of Sabina & members of the team. Please reach out to Sabina for expert assistance with your gig.

The Self-Discovery Challenge

Rather than tell you what I think these problems are and how they might be solved, I've created something better: a framework for discovering it yourself through guided analysis with AI.

Because here's what I've learned after five decades in this space: until you've identified and fully understood the nature of the problem and the pain it creates for systems and people then reasoned through these challenges of fixing them with a Mutual Credit system yourself, you'll keep believing that your particular approach is the one that will finally work. The pattern recognition only comes through your own analytical journey. If you become interested in that then join up for the free subscription to hear how to use the tools I have created and taught to achieve the meaningful outcomes, you have imagined.

The Prompts That Changed Everything

I've developed a sequence of AI prompts that guide you through the same analytical journey that took me decades to complete. You'll explore:

Why cooperative movements consistently face the same behavioral challenges

How credit systems create unintended incentive structures

What happens when small-scale trust networks try to scale

How technology interacts with human psychology in exchange systems

What types of remedies would actually need to be created

The beauty of this approach is that you'll reach conclusions through your own reasoning, not just accept someone else's experience. And because you're working with AI, you can explore scenarios and test assumptions in ways that weren't possible when I was learning these lessons the hard way.

Why This Matters Now

We're standing at a unique moment in history. The combination of:

Distributed computing power (Holochain, blockchain)

Artificial intelligence (for handling complexity)

Global connectivity (for network effects)

Economic disruption (creating demand for alternatives)

...might finally give us the tools to solve problems that have plagued cooperative movements for generations.

But only if we understand what we're really up against.

Your Turn to Explore

If this subject interests you, why not start with a discussion with your AI to discover what these problems are and what types of remedies would have to be created to make a mutual credit system work?

I hope you have as much fun as I did creating the prompts. More importantly, I hope your analysis reveals insights that my fifty years of experience missed.

Because the next breakthrough in alternative exchange systems won't come from repeating old patterns with new technology. It will come from understanding why those patterns persist - and designing systems that work with human nature instead of against it.

Ready to dive in? The complete AI analysis framework is below. It represents five decades of questions distilled into a few hours of guided discovery.

The future of cooperative economics might just depend on what you discover.

[Include the complete prompt framework here]

After you complete your analysis, I'd love to hear what you discovered. Did it confirm my experience, or reveal new possibilities I've missed? The next generation of builders stands on the shoulders of those who came before - but sometimes they see further than we ever could.

Self-Discovery Analysis: Mutual Credit Systems Reality Check

For Developers, Entrepreneurs, and Web3/Blockchain Builders

Before you invest time and resources into building another mutual credit system, conduct this critical analysis to understand what you're really up against.

How to Use These Instructions

Copy and paste the prompts below into Claude (or similar AI) along with the provided research context. Work through them in sequence - each builds on the previous analysis. The goal is for you to discover the real challenges through your own reasoning, not just accept someone else's conclusions.

Required Context (Copy This First)

[Paste the entire contents of the research document provided - the table of root problems in mutual credit systems]

Prompt Sequence for Self-Discovery

Prompt 1: Initial Assessment

I'm considering building a mutual credit system using [Web3/blockchain/Holochain/AI - specify your platform]. Based on the research provided and your knowledge, help me understand what I'm really trying to achieve.

Please analyze:

1. What is the core promise that mutual credit advocates make about these systems?

2. What would success actually look like in concrete terms?

3. Given the research, what patterns do you notice about why previous attempts haven't achieved this success?

Be honest and critical - I want to make informed decisions, not chase unrealistic dreams.Prompt 2: Scale Analysis Challenge

Now I want to stress-test the scaling assumptions. Assume I successfully launch a mutual credit system that works well with 50 committed users in a tight-knit community.

Walk me through what happens as I try to grow to:

- 500 users (mixing strangers with the core community)

- 5,000 users (mostly anonymous participants)

- 50,000 users (regional scale)

- 500,000+ users (competing with mainstream financial systems)

At each stage, identify what new problems emerge and why. Focus on the human behavior and system dynamics, not just technical challenges.Prompt 3: Technology Reality Check

I believe my chosen technology platform [Web3/blockchain/Holochain/AI/etc.] can solve the problems that caused previous mutual credit systems to fail.

Challenge this assumption. For each major problem identified in the research:

1. How specifically would my technology solve it?

2. What new problems might my technology create?

3. Are there fundamental issues that no technology can solve?

4. What would I need to prove before claiming my approach is different?

Be skeptical - assume I'm suffering from "technology will solve everything" bias.Prompt 4: Economic Incentive Analysis

Help me map out the economic incentives in my proposed system from multiple perspectives:

For each type of participant (early adopters, businesses, casual users, potential bad actors):

1. Why would they join initially?

2. Why would they stay active long-term?

3. Under what conditions would they leave or exploit the system?

4. How do their incentives change as the network grows?

Then identify any misaligned incentives that could undermine the system's goals.Prompt 5: Competitive Analysis

My mutual credit system will be competing with:

- Fiat currency and traditional banking

- Credit cards and digital payments

- Crypto currencies

- Existing community currency systems

- Barter and informal exchange

For each competitor, analyze:

1. What advantages do they have that I don't?

2. What switching costs exist for users?

3. Under what specific circumstances would people choose my system over these alternatives?

4. How do these competitive dynamics change as my system tries to scale?

Be brutally honest about when and why people would actually use this.Prompt 6: Comprehensive Problem Assessment

Based on all our previous analysis, create a comprehensive table showing:

| Critical Problem | How It Manifests | Why Technology Alone Won't Fix It | What Would Actually Need to Be Solved |

Include problems we've identified through our analysis, plus any from the original research that we haven't fully addressed. Focus on root causes, not symptoms.

After the table, provide your assessment: Has any existing mutual credit system successfully solved all these problems simultaneously? What would it take to do so?Prompt 7: Investment Decision Framework

Given everything we've analyzed, help me create a decision framework:

1. What specific evidence would I need to see before believing my approach could succeed where others have failed?

2. What would I need to prototype and prove before investing serious resources?

3. What are the most likely failure modes, and how would I know early if I'm heading toward them?

4. What alternative approaches might achieve my underlying goals more effectively?

End with: Based on this analysis, what would you recommend I do next?Important Notes for Best Results

Be Specific: Replace [Web3/blockchain/Holochain/AI] with your actual chosen platform

Stay Engaged: Challenge Claude's responses if they seem too optimistic or pessimistic

Ask Follow-ups: If something isn't clear, ask for examples or deeper explanation

Document Insights: Keep notes as you go - patterns will emerge across the prompts

Be Honest: The goal is truth-seeking, not confirmation of your existing beliefs

What You Should Discover

If you work through this analysis honestly, you should reach some uncomfortable realizations about:

The gap between mutual credit promises and reality

Why "this time is different" thinking is usually wrong

What it would actually take to build a viable system

Whether your time and resources might be better invested elsewhere

Final Reality Check

After completing this analysis, ask yourself:

Am I still confident this is the right approach?

What specific evidence changed my thinking?

What would I need to see to justify moving forward?

What alternative approaches should I consider?

The goal isn't to discourage innovation, but to ensure you're solving real problems with viable solutions rather than recreating well-documented failures with new technology.

These prompts are designed to help you think critically and discover insights through your own reasoning. The conclusions you reach will be more valuable because you arrived at them yourself.

Whoah - just did the prompting as suggested - extremely useful. Thank you Stephen.